.svg)

10 Best Financial Consolidation Software Solutions for UAE Businesses in 2026

A practitioner's read on Gartner's latest Magic Quadrant for Financial Close and Consolidation Solutions, translated for groups operating across the UAE and GCC.

Why this matters here

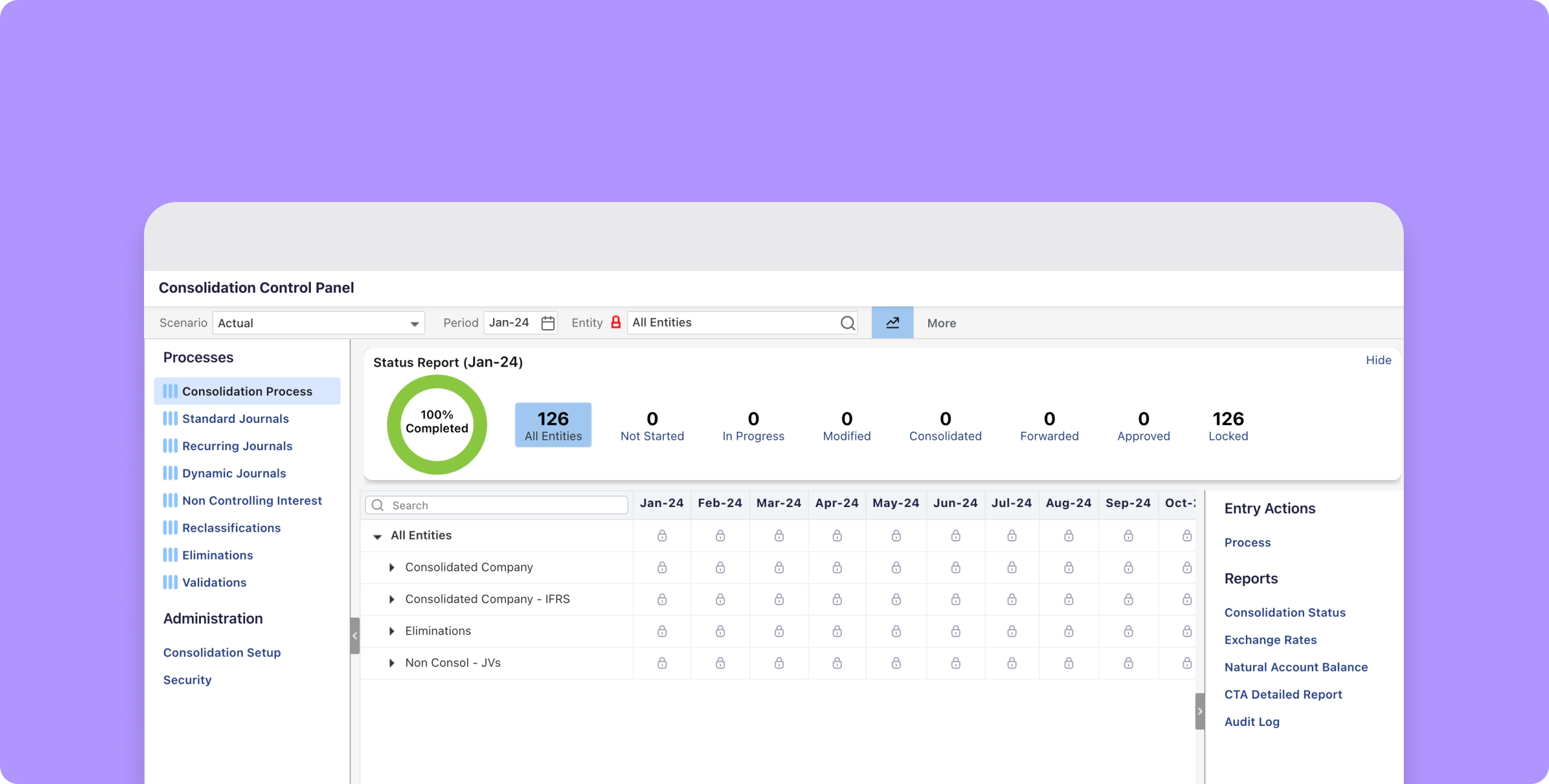

Most consolidation problems in the UAE aren't really software problems. They're structure problems that software eventually has to absorb. A holding company with three free zone entities, a mainland trading license, and a subsidiary in Riyadh doesn't need "a tool," it needs an engine that can handle intercompany eliminations, multiple ownership percentages, and currency translation without someone rebuilding a workbook every quarter.

Three regulatory realities are pushing this decision faster than usual right now: Corporate Tax has made documentation and audit trails non-negotiable, the FTA's e-invoicing mandate (Peppol network, PINT-AE format) is forcing structured data at the transaction level rather than after the fact, and most groups here aren't UAE-only. They're managing Saudi entities under ZATCA, sometimes Jordan under JoFotara. A consolidation platform that only thinks in single-country terms doesn't survive contact with a real GCC group structure.

Gartner's March 2026 Magic Quadrant for FCCS is the best independent read on this market right now. What follows is that research filtered through what actually matters for a UAE-based finance function: multi-entity ownership handling, IFRS/GAAP flexibility, ERP connectivity, and realistic support coverage in this time zone.

What to actually check before you shortlist anyone

- Ownership and FX engine: can it recalculate noncontrolling interests automatically when a stake changes, or does someone rebuild the hierarchy by hand?

- Standards flexibility: IFRS locally, possibly GAAP or another standard for a foreign parent, from the same trial balances.

- Intercompany data quality upstream: e-invoicing itself sits in the ERP's AP/AR layer, not in FCCS, but structured invoice data (Peppol/PINT-AE, ZATCA, ETA, JoFotara) flowing in cleanly makes intercompany elimination and audit trails easier downstream.

- ERP fit: NetSuite, Odoo, or SAP connectivity that doesn't require a custom integration project.

- Where AI is priced: several vendors below now separate agentic/AI features into their own pricing tier. Get the three-year number, not the year-one number.

Market positioning at a glance

1. Oracle EPM (Fusion and NetSuite). Leader

Automated chart-of-accounts mapping is the real value here. It harmonizes data from whatever mix of legacy on-premises and cloud ERPs your subsidiaries happen to run, which is more common than anyone admits in a group that's grown by acquisition. Single per-user pricing across modules keeps budgeting simple. The trade-off: Oracle's out-of-the-box approach isn't built for heavily customized transaction matching, and iXBRL-style filing goes through a partner, not natively.

We've deployed Oracle NetSuite EPM alongside NetSuite implementations for GCC groups at Azdan, and the pattern holds true in the field: the consolidation and close functionality is genuinely strong once the chart-of-accounts mapping is set up correctly, but that initial mapping exercise across free zone, mainland, and cross-border entities is where projects gain or lose time. Budget for it properly during scoping rather than treating it as a formality.

2. OneStream. Leader

The embedded data-quality engine validates figures before they enter consolidation, which matters when you're pulling from several GCC ledgers of varying quality. Its GAAP-to-IFRS bridge is genuinely useful if you're reporting IFRS locally but rolling up to a US or European parent under a different standard. Watch for the AI features sitting on a separate pricing tier, and iXBRL filing again requires a partner.

3. Wolters Kluwer, CCH Tagetik. Leader

Strong disclosure management and industry starter kits for banking and insurance, relevant given the DIFC/ADGM-regulated population here. The GenAI review layer catches missing disclosures before an auditor does. Configurability is a double-edged sword: powerful for complex groups, slower to deploy for smaller ones without dedicated technical resources.

4. BlackLine. Challenger

Every consolidated number traces back to its source transaction, the feature that actually earns its keep during a VAT audit or Corporate Tax review. The Verity AI layer exposes its own reasoning rather than acting as a black box. Some mid-market customers find pricing and BlackLine's standardized governance model require more process change than expected. Run a proof-of-concept before committing.

5. Anaplan. Challenger

The time-based ownership engine is the standout: noncontrolling interests recalculate automatically as stakes change, which is exactly what a holding company mid-acquisition across the GCC needs. AI-assisted data mapping speeds up onboarding new entities. Journal entry functionality has real gaps around FX translation detail today, and AI pricing is expected to shift from free to usage-based.

6. Board. Challenger

One platform for close, consolidation, and planning. Useful if you're tired of stitching two systems together. IFRS, ESG, and Pillar Two accelerators are built in. No native bank/subledger reconciliation, so pair it with something else if that's a heavy need, and local jurisdiction templates need manual configuration.

7. HighRadius. Challenger

Twenty-plus ML models flag GL anomalies before close starts, not after. The outcome-based engagement model, where the vendor commits to KPI improvements, is a rare and useful structure if you need to justify the spend internally. Support footprint is still concentrated in North America; confirm GCC coverage before signing.

8. Planful. Challenger

Low-code administration means your finance team can run this without a dedicated developer. The right call for leaner UAE mid-market functions. Comprehensive transaction matching still runs through third-party partnerships rather than natively, and the customer base skews North American, so push on GCC implementation references.

9. Vena. Niche Player

Built on an Excel-like interface, which cuts change-management friction for teams that already live in spreadsheets. Effective-dated ownership rules handle recalculations automatically. Reconciliation is intercompany-only today, not full balance-sheet matching, and several AI-first workflow features are still on the roadmap rather than shipped.

10. Prophix. Niche Player

Handles hundreds of legal entities without heavy IT dependency. Relevant for the sprawling free zone/mainland structures common here. Usage-based pricing with AI included keeps costs predictable. No native Teams/Outlook integration for workflow notifications yet, and retention rates, while improving, still trail the market. Ask for references.

Worth a mention if you're ERP-first

Oracle NetSuite, SAP Cloud ERP Group Reporting, and Workday Financial Management all offer embedded consolidation but weren't evaluated as standalone FCCS platforms by Gartner. If you're already on NetSuite, the honest first question is whether a native or connector-based consolidation layer solves your problem before you add a separate platform on top.

Bottom line

Pick based on your entity structure, not the ranking. Acquisitive groups with shifting ownership stakes lean toward Anaplan or Board. Regulated banking/insurance entities get more out of Tagetik's starter kits despite the setup overhead. Leaner mid-market groups get to value faster with Planful, Vena, or Prophix. Whatever you choose, push hard on three things during procurement: e-invoicing roadmap across the GCC, multi-entity ownership handling, and exactly what the AI features will cost once the free tier ends.

Based on Gartner's "Magic Quadrant for Financial Close and Consolidation Solutions" (9 March 2026, ID G00835009). Full report and official graphic: licensed reprint at https://www.gartner.com/doc/reprints?id=1-2MZ16LVL&ct=260311&st=sb. Gartner does not endorse any vendor depicted in its research.